News:

Long Island

Posted: December 3, 2019

Commercial Classroom: 1031 exchange “basics” - by Edward Smith

This column is offered to help educate agents new to commercial and investment brokerage and serve as a review of basics for existing practitioners.

This column is offered to help educate agents new to commercial and investment brokerage and serve as a review of basics for existing practitioners.

The sale of real estate held for more than 12 months triggers capital gains taxes on the net profits of that sale. These taxes may be deferred by participating in a 1031 tax exchange, in essence, by purchasing property(s) to replace the one(s) being sold. However, there are stringent rules and timetables that must be complied with. This applies to the sale of commercial or investment property, but not your personal residence.

The entity that conducts the 1031 exchange is known as a Qualified Intermediary (QI). The IRS requires that a “third party” conducts the exchange so the QI will act as a principal in the transaction. How it basically works: The taxpayer will relinquish property title (of the property being sold) to the QI, who will actually sell the property and hold the sale proceeds. Then the QI will act as the buyer of the replacement property being purchased.

The QI prepares all the required documentation, provides complete accounting to the taxpayer and concludes by transferring the title of the new acquired property to the taxpayer.

A few interesting points about QIs. Currently there are no licensing requirements. QI cannot be the taxpayer. The taxpayer’s accountant, attorney and real estate agent, who worked with the taxpayer during the prior two years, are disqualified from serving as the QI.

Qualified Properties

Replacement property acquired in an Exchange must be like-kind to the property being relinquished. Like-kind means “similar in nature or character, notwithstanding differences in grade or quality.” Both the relinquished and the replacement properties must be held by the exchanger for investment purposes or for “productive use in their trade or business.” Personal property is not eligible for exchange.

General Rules

- Identify the replacement property within 45 days after transfer of the relinquished property.

- Receive title to the replacement property within 180 days after the transfer of the relinquished property.

- All proceeds of the sale of the relinquished property must be held by a third party, a QI.

- All cash proceeds must be invested to fully defer taxable gain.

Three Acquisition Rules

- The “Three-Investment Property Rule” states that the exchanger must identify up to, but no more than three potential investment properties during the acquisition period; OR

- The “Two Hundred Percent Rule” rule dictates that, in the event that three or more like-kind investment properties are selected as replacement investment properties, the aggregate market value of said investment properties may not exceed 200% of the market value of relinquished investment property; OR

- The “Ninety-Five Percent Exception” In the even that rules 1 and 2 do not apply, the Ninety-Five Percent Exception takes precedence. This rule dictates that the aggregate market value of all replacement investment properties must represent at least 95% of the value of the relinquished investment properties in order for the exchange to still qualify.

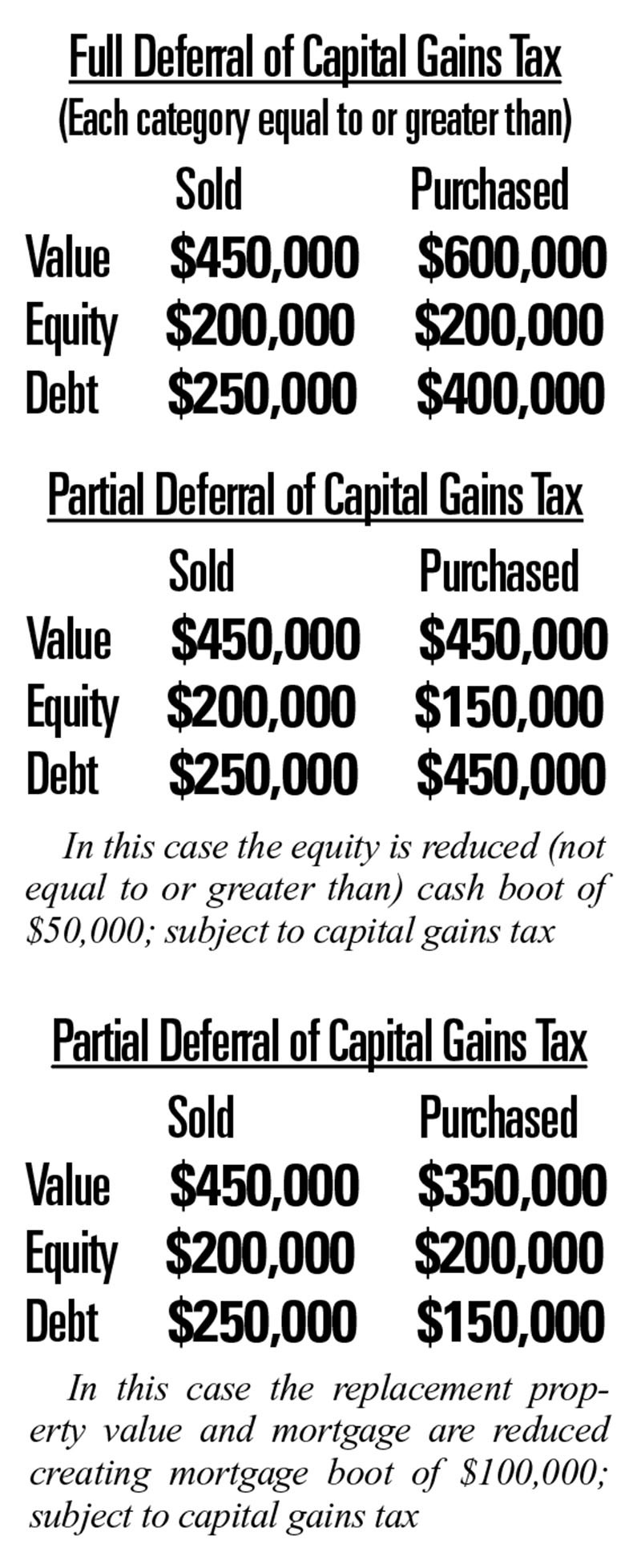

Full and Partial Exchanges

When all the proceeds of the sale are used to purchase a replacement property and the value, equity and debt are all “equal to or greater than” a full deferral of the capital gains tax is possible. If all these rules are not complied with a partial deferral of the taxes may be possible.

“Boot,” is a term used to describe other non-qualified property received in an exchange, that is not like kind to the property acquired (cash, stock, personal property). The “boot” proceeds in the exchange are considered a gain and are taxable. For a full deferral of capital gains taxes the value, equity and debt must be “equal to or greater than.”

As one can see 1031 tax deferred exchanges can be very beneficial, but they are complicated with many rules (only some of which we have examined in this article). There are many different types of exchanges and clients need to speak with a specialist, a QI.

Edward Smith, Jr., CREI, ITI, CIC, GREEN, MICP, CNE, is a commercial real estate consultant, instructor and broker at Smith Commercial Real Estate, Sandy Hook, CT.

Tags:

Long Island

MORE FROM Long Island

Suffolk County IDA supports expansion of A&Z Pharmaceuticals

Hauppauge, NY The Suffolk County Industrial Development Agency (IDA) has granted preliminary approval of a financial incentive package that will assist a manufacturer in expanding its business by manufacturing more prescription (Rx) pharmaceuticals in addition to its existing over-the-counter