News:

Brokerage

Posted: May 7, 2019

Question of the Month: Can a zoning lot consisting of more than one tax lot include partial tax lots, or must it include the full lot? - by Christopher Wright

Capell Barnett Matalon & Schoenfeld LLP

There was a recent Manhattan Supreme Court decision regarding the definition of a zoning lot. The matter involved three proceedings. First, an application was submitted to the Dept. of Buildings seeking permits to construct a 55-story residential building based on a zoning lot that included partial tax lots. Second, the zoning lot was appealed to the Board of Standards and Appeals (BSA) alleging that the zoning lot’s use of partial tax lots did not comply with zoning regulations. Third, after the BSA upheld the zoning lot, a lawsuit was filed alleging that the zoning lot was faulty and that the BSA was in error. The court reversed the BSA.

Although these proceedings involved complex zoning arguments, the central issue is relatively straight forward. The question to be decided is: Can a zoning lot that consists of more than one tax lot (a “combined zoning lot”) include a portion of another tax lot or must it include the entire tax lot?

Tax lots are combined into a single zoning lot for the purpose of transferring development rights or other zoning requirements between the tax lots to achieve a more efficient development scenario.

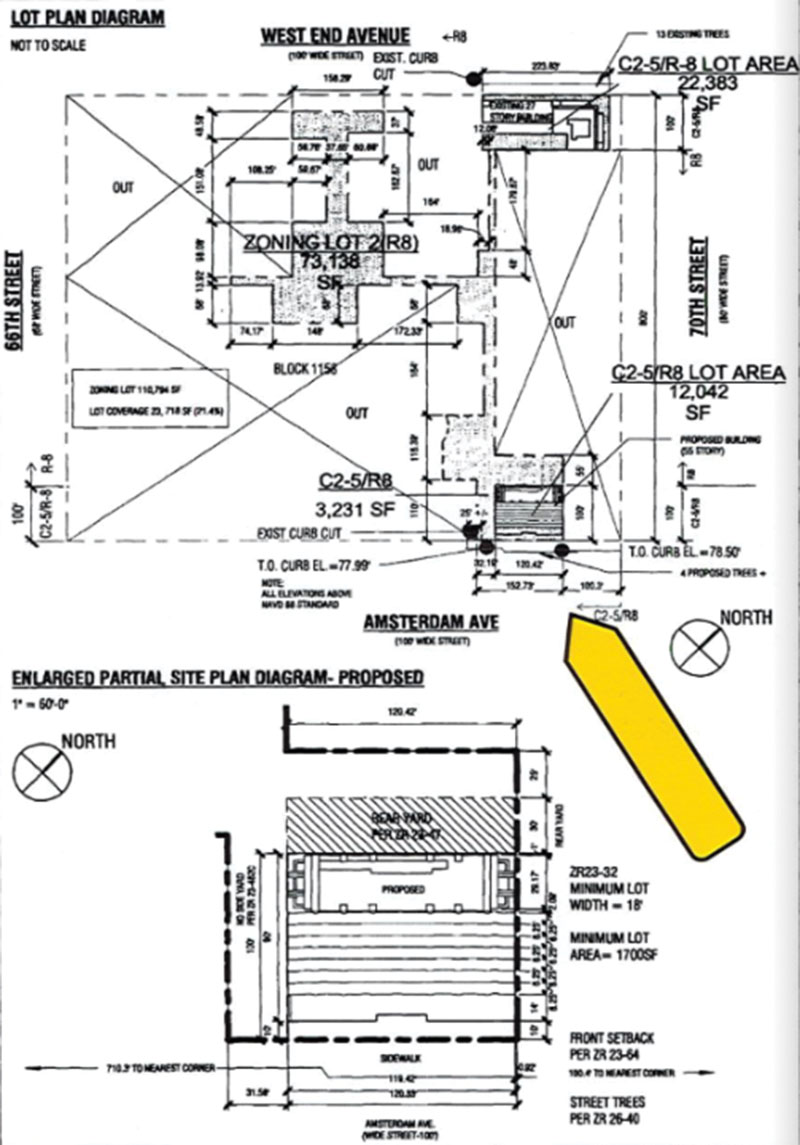

The combined zoning lot was being used to construct a 55-story building located at 200 Amsterdam Ave. that abuts the Lincoln Towers residential complex located between Amsterdam and West End Aves. between 66th and 70th Sts. Lincoln Towers houses several thousand apartments and has large open areas between the buildings that are used as yards and driveways for the residents.

The developer of 200 Amsterdam Ave. was looking to create a combined zoning lot to transfer development rights and open space. The transfer of development rights was significant, totaling over 200,000 s/f of floor area. The open space transfer was to provide the required open space to develop the transferred development rights.

The developer of 200 Amsterdam Ave. was looking to create a combined zoning lot to transfer development rights and open space. The transfer of development rights was significant, totaling over 200,000 s/f of floor area. The open space transfer was to provide the required open space to develop the transferred development rights.

Certain residential zoning districts do not have building height limits. These are called height factor buildings. Height factor requires a series of setbacks as the building goes higher, causing the building to taper at the higher floors. However, as the building grows–goes higher–more open space is required, the theory being that taller buildings must be narrower to allow light and air to reach the ground.

The Zoning Diagram of the proposed building submitted to DOB demonstrated that a tapering 55-story building could be built on the development site using the height factor zoning envelope. However, the development site was not large enough to provide the required open space. To solve this problem a combined zoning lot was created that included portions of the Lincoln Tower open areas, including yards and driveways. These open areas were located on portions of various tax lots. The combined zoning lot allowed the development site to claim these open areas as satisfying the open space requirement for the 55-story building. Essentially, the open areas created on the Lincoln Tower complex were transferred to the development site, not physical like development rights, but for the purpose of satisfying open space zoning calculations.

The development site is at the corner of West 69th St. and Amsterdam Ave. As shown on the zoning diagram, the combined zoning lot basically extends tentacles from the development site to encircle the Lincoln Towers yards and drive ways. The combined zoning lot crosses several of the Lincoln Towers tax lot lines to reach the open areas.

During these proceedings, the parties on both sides referenced numerous zoning regulations that used the terms “zoning lot” and “tax lot.” The proponents of partial tax lots argued that the zoning regulations were vague and never explicitly stated that a combined zoning lot must always include the entire tax lot. The parties in opposition argued that the plain language of the zoning regulations clearly inferred that full tax lots must be included in any combined zoning lot.

The proponents also referenced a DOB memorandum (the “Minkin Memo”), written in 1978, that stated that zoning lots could include “parts of tax lot” and argued that this had been the standard interpretation for 50 years. The developer identified 34 examples of zoning lots containing partial tax lots. However, the court distinguished all of these lots as applying to special circumstances not applicable to the subject zoning lot. Interestingly, although the BSA upheld the use of partial tax lots, the BSA did not reference any of these examples as legal justification for its decision, instead relying on the language of the zoning regulations. DOB supported the zoning lot (DOB had issued the permits) but opined that the Minkin Memo was in error and a revised DOB memo would be issued requiring full tax lots. The court gave great weight to DOB’s pending retraction of the Minki Memo.

In my experience, I have never dealt with a zoning lot using partial tax lots. The intent of zoning is to locate required open areas in proximity to the building for the purpose of providing an amenity to the residents of the building. Here, the open areas had no physical relationship to the 55-story building. Open space designed for use by Lincoln Towers was being used to give the proposed building open space credits. The proposed building was not creating any new open space.

Christopher Wright is of counsel at Capell Barnett Matalon & Schoenfeld LLP, New York, N.Y.

Tags:

Brokerage

MORE FROM Brokerage

Elecor Properties executes 150,000 s/f of leases at One Market Plaza

San Francisco, CA Elecor Properties has secured four leases comprising 149,914 s/f at One Market Plaza since the beginning of the year, underscoring strong demand for premier office

Quick Hits

Columns and Thought Leadership

The death of the generic offering memorandum: What buyers expect in 2025 - by Kimberly Zar Bloorian

There was a time when an offering memorandum (OM) was pretty bare bones, some photos, a few bullet points on income, and a rent roll thrown in at the back. That used to get the job done. Not anymore. In 2025, buyers are sharper, faster, and more selective. They’re looking

The anticipated effect of Basel III and ISO 20022 implementation on commercial real estate - by Michael Zysman

July 1, 2025 is the deadline for US banks to begin to adopt Basel III banking standards and July 14, 2025 is the deadline for U.S. banks to adopt ISO 20022 messaging standards. Both will have a significant effect on the banking and commercial real estate (CRE) finance sectors.

Tri-state capital migrates nationally amid regulation pressure - by Reese Weaver

New York tri-state multifamily investors are increasingly reallocating capital to less-regulated markets across the U.S. as rent control and legislative risk erode returns at home. With over 60% of New York City’s rental housing stock classified as rent-stabilized, the traditional value-add model — buying under-performing buildings,

A fresh start - by Shallini Mehra and Amit Doshi

For the past several years, the New York City multifamily housing market has been defined by disruption. The combined impact of the HSTPA rent laws and a sharply higher interest rate environment has fundamentally reduced

.gif)